Abortion protection was a key difficulty within the debate main as much as the passage of the Reasonably priced Care Act. Once more, it could possibly be a problem if Congress considers extending the enhanced premium tax credits that can expire by the top of the yr absent Congressional motion. With out the extension of those enhanced premium tax credit, out-of-pocket premiums would rise by over 75% on common for the overwhelming majority of people and households shopping for protection by the ACA Marketplaces resulting in an estimated 3.8 million extra folks turning into uninsured as they drop their protection over the following 10 years. Anti-abortion advocates are presently urging Congress to ban any premium tax credit for use in direction of any plans that embrace abortion protection. This coverage watch explains how abortion protection works in ACA Market plans, state actions to incorporate or exclude abortion protection in these plans, and the potential impression if Congress bans abortion protection in all Market plans.

The ACA Explicitly Says that Federal Funds Could Not Be Used to Pay for Market Abortion Protection Past the Hyde Limitations

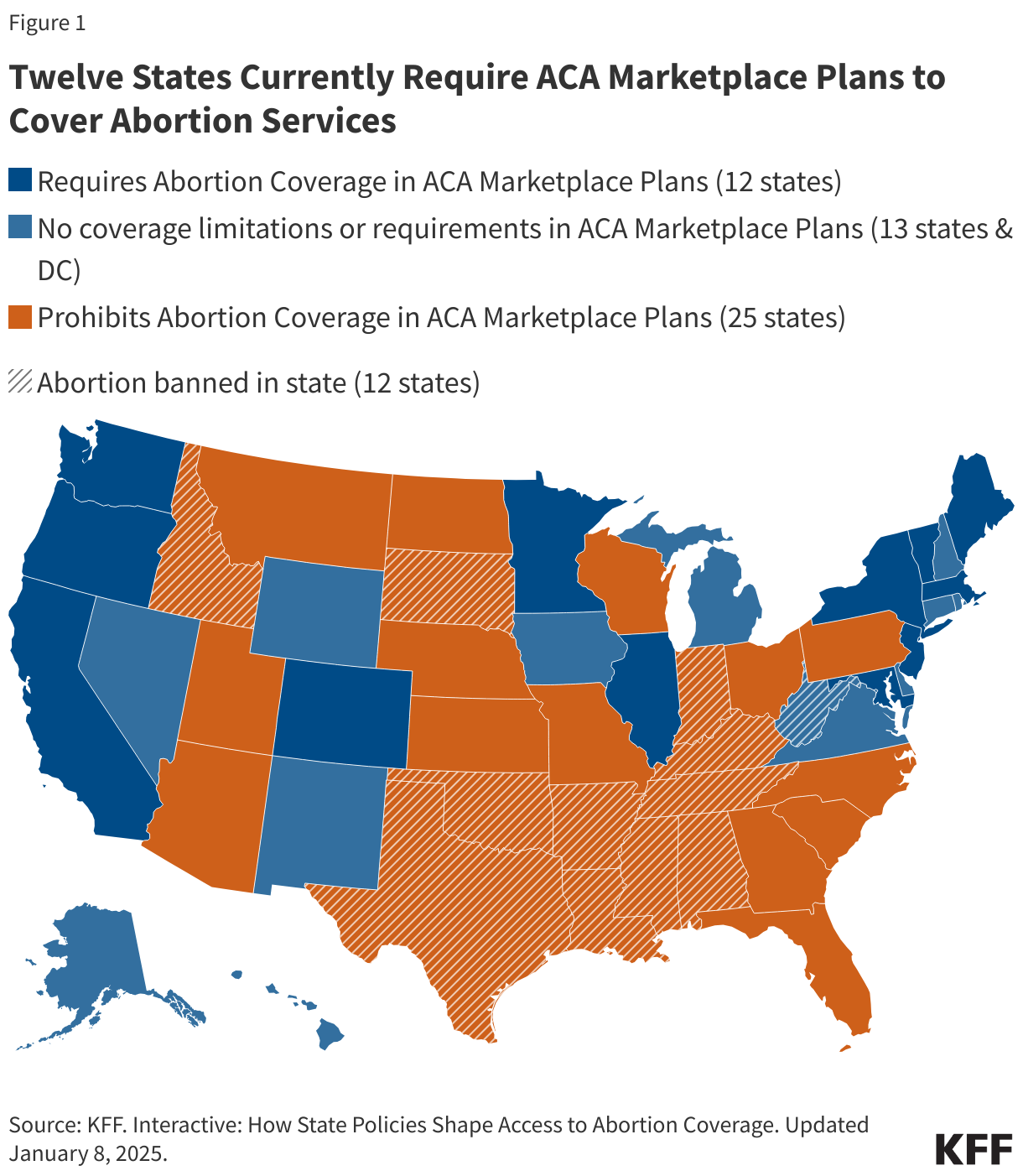

The ACA statute has particular language that applies Hyde Modification restrictions to the usage of premium tax credit, limiting them to utilizing federal funds to pay for abortions solely in instances that endanger the lifetime of the girl or which are a results of rape or incest. The ACA additionally explicitly permits states to bar all plans collaborating within the state Market from protecting abortions, which 25 states have achieved for the reason that ACA was signed into legislation in 2010. Alternatively, twelve states now have legal guidelines that require all fully-insured group plans and particular person plans (together with Market plans) to incorporate abortion protection. 13 states and DC neither require nor prohibit abortion protection in Market plans (Determine 1). Federal legislation prohibits Market plans from providing any riders, a supplemental profit coverage that covers sure companies which aren’t included in an ordinary medical insurance plan. So, if a plan doesn’t embrace abortion protection, an enrollee can not purchase a rider for abortion protection.

ACA Guidelines for Premiums for Abortion Protection

In states that don’t bar protection of abortions on plans out there by the Market, insurers could supply a plan that covers abortions past the permissible Hyde modification conditions when the being pregnant is a results of rape, or incest or the pregnant particular person’s life is endangered. , however this protection can’t be paid with federal {dollars}. Plans should notify customers of the abortion protection as a part of the abstract of advantages and protection rationalization on the time of enrollment. The ACA outlines a strategy for states to observe to make sure that no federal funds are used in direction of protection for abortions past the Hyde limitations. Any plan that covers abortions past Hyde limitations should estimate the actuarial worth, the quantity the plan expects to pay on behalf of its members on common, of such protection by taking into consideration the price of the abortion profit (valued at least $1 per enrollee per month). The legislation says that this estimate can not bear in mind any financial savings that is likely to be achieved because of the abortions (similar to prenatal care or supply).

The Anti-Abortion Advocates’ Declare That Federal Funds Are Subsidizing Abortion Protection

Abortion opponents are claiming that federal funds are getting used to subsidize abortion as a result of they imagine these subsidies allow people to have protection by the ACA Market that features abortion protection, despite the fact that plans should cost every enrollee a $1 monthly to pay for the prices of coated abortions and segregate these funds from different premium funds. Whereas the anti-abortion advocates declare that the requirement for plans to segregate premiums for abortion protection is an “accounting gimmick,” the required minimal of $1 per member monthly that’s specified within the ACA is greater than issuers estimate to be the actuarial value of the premium attributable to the price of abortion protection. In different phrases, the $1 month cost per enrollee (no matter age or gender) exceeds the price of abortions that plans are paying for with these funds. For instance, a current evaluate confirmed that Maryland plans have been holding $25 million in unspent funds from policyholder funds for segregated premiums for abortion protection and it is extremely seemingly that plans in different states have surplus funds which were collected for abortion protection.

What Would Be the Impression if Congress Bans Premium Tax Credit for Plans that Embrace Abortion Protection?

Twelve states require plans that aren’t self-insured to cowl abortion. If Congress have been to ban the usage of premium tax credit for Market plans that embrace abortion protection past the Hyde restrictions, people in these 12 states wouldn’t have the ability to use federal tax credit to acquire protection in a Market plan. In 2023, approximately 3.7 million folks have been enrolled in ACA market plans within the 12 states that require abortion protection. As well as, it is going to additionally have an effect on folks within the 13 states and DC that enable abortion protection however don’t mandate it. Whereas Democrats could not comply with a ban on the supply of ACA premium taxes for plans that cowl abortion, the dearth of a ban might make it tougher to draw Republican help for an extension of the improved tax credit.