ACA premium tax credit, which make medical insurance Market plans extra reasonably priced, have been first enhanced as part of the American Rescue Plan Act in 2021 after which prolonged by Congress by 2025. The improved credit have improved insurance coverage protection affordability for tens of millions of individuals, together with these with HIV. Nonetheless, they’re at present set to run out on the finish of the yr, until Congress acts to increase them. Their extension grew to become a significant political issue taking part in a job within the authorities shutdown. As well as, due to the political uncertainty surrounding their extension, well being insurers have proposed premium increases past what would in any other case be the case. The lack of the improved tax credit, coupled with elevated premiums for some, might jeopardize protection or well being care affordability for tens of millions. Folks with HIV could also be significantly susceptible, on condition that they’re more likely to have Market plans than the general public total and lots of additionally depend on the federally-funded Ryan White HIV/AIDS Program, which might be additional stretched if Market plans grow to be costlier. Furthermore, lack of protection and elevated prices might result in disruptions in take care of individuals with HIV which might have critical implications for particular person and public well being. Being engaged in HIV care, together with being on antiretroviral remedy, promotes optimal well being outcomes together with viral suppression, which in flip prevents transmission of HIV to others. This problem transient supplies an summary of those potential impacts.

Folks with HIV and Market Protection

A larger share of individuals with HIV obtain protection by the Marketplaces than the overall inhabitants. As with Market enrollees total, the prices they face might rise considerably if the tax credit should not prolonged (element on how the improved tax credit are calculated and differ from the unique ACA tax credit score here). For instance:

- State of affairs 1: A forty five-year-old enrolled in a Market plan in Miami-Dade County, FL with an annual earnings of $38,000 (243% of the federal poverty degree (FPL)), demographics much like the HIV epidemic total, would pay an estimated $1,699 extra per yr for protection for the second lowest value silver plan, with the month-to-month premium going from $117 to $259. (Further situations will be run utilizing this KFF interactive tool.)

Individually, these with incomes over 400% of the FPL (estimated at $62,600 in 2026 for a single-individual family) would face a double hit in terms of value will increase with out an extension. First, individuals with incomes on this vary have been supplied with a brand new tax credit score, limiting premium prices to eight.5% of earnings, which they might lose totally with out an extension. Second, with none cap on prices, they might be totally uncovered to elevated premiums proposed for 2026. (This differs from these within the 100%-400% FPL earnings group who would nonetheless obtain some federal help, albeit at a decrease degree than with the improved credit.)

- State of affairs 2: A forty five-year-old enrolled in a Market plan in Miami-Dade County, FL with an annual earnings of $65,000 (415% of the federal poverty degree (FPL)), would pay an estimated $2,027 extra per yr for protection for the second lowest value silver plan, with the month-to-month premium going from $460 to $629. (Further situations will be run utilizing this KFF interactive tool.) Prices would go from being caped at 8.5% of their earnings to consuming 11.6%

Sure state enrollees are already going through particularly giant hikes. Wanting on the 5 states with the best HIV prevalence the, median and range requested premium increases for the 2026 plan yr are as follows:

- CA: 14% (7%-20%)

- FL: 26% (19%-41%)

- GA: 20% (9%-43%)

- NY: 13% (10%-37%)

- TX: 19% (3%-42%)

There are a number of potential impacts of elevated premium prices for people with HIV paying for their very own protection. Whereas some individuals could retain protection, and be capable of handle the elevated prices, others might:

- Retain protection and wrestle with the elevated prices.

- Select a plan with cheaper premiums, however doubtlessly increased out-of-pocket prices for objects like HIV medicines, labs, and supplier visits.

- Drop protection altogether and never search various entry to care or protection.

- Drop protection and search assist from the Ryan White Program.

AIDS Drug Help (ADAPs) Applications

Notably, HIV packages would even be impacted if enhanced tax credit should not prolonged, with the coverage lapse costing them doubtlessly tens of tens of millions of {dollars}. That is particularly the case for AIDS Drug Help Applications (ADAPs), that are a part of the Ryan White HIV/AIDS Program, a federal security web program for these with low-to-moderate incomes, reaching over half of individuals with HIV within the U.S. ADAPs present HIV medicines to individuals with HIV both instantly or by buying insurance coverage protection with prescription drug advantages on their behalf and/or aiding with cost-sharing of insurance coverage protection. Every state/territory runs its personal ADAP and packages differ of their operation and providers supplied. ADAPs face restricted budgets and federal allocations have been pretty flat over time, making this system susceptible to modifications within the measurement of the inhabitants needing providers in addition to the price of these providers. ADAPs hit with rising premiums or elevated enrollment, might be confronted with modifying their packages in ways in which might impede entry.

Insurance coverage buying grew to become more widespread as soon as the ACA was signed into legislation as traditionally HIV had been an uninsurable situation within the particular person market. The well being legislation meant that individuals with HIV couldn’t be denied protection or charged extra for being HIV constructive and that they have been assured comparatively protection entry to needed medicines and coverings.

Most ADAPs buy personal insurance coverage premiums for purchasers (a minimum of 42 states and DC in 20231). In complete, in 2023 a minimum of 76,365 purchasers have been assisted with insurance coverage help that included assist paying for premiums throughout insurance coverage markets. Amongst all ADAP purchasers, over 40,0002 have been enrolled in Market plans in 2023 and most acquired insurance coverage assist from this system. ADAPs that enroll eligible purchasers in Market plans obtain the good thing about the tax credit (at present accessible to these 100% of the poverty degree and above) and have processes in place to work with purchasers on tax credit score reconciliation on the finish of the yr. Larger shares of ADAP purchasers receiving premium assist 3 have incomes above 100% FPL (the earnings degree at which tax credit score eligibility begins) in comparison with these enrolled in full-pay drug assist solely.

How a lot might the lack of enhanced tax credit value state ADAPs?

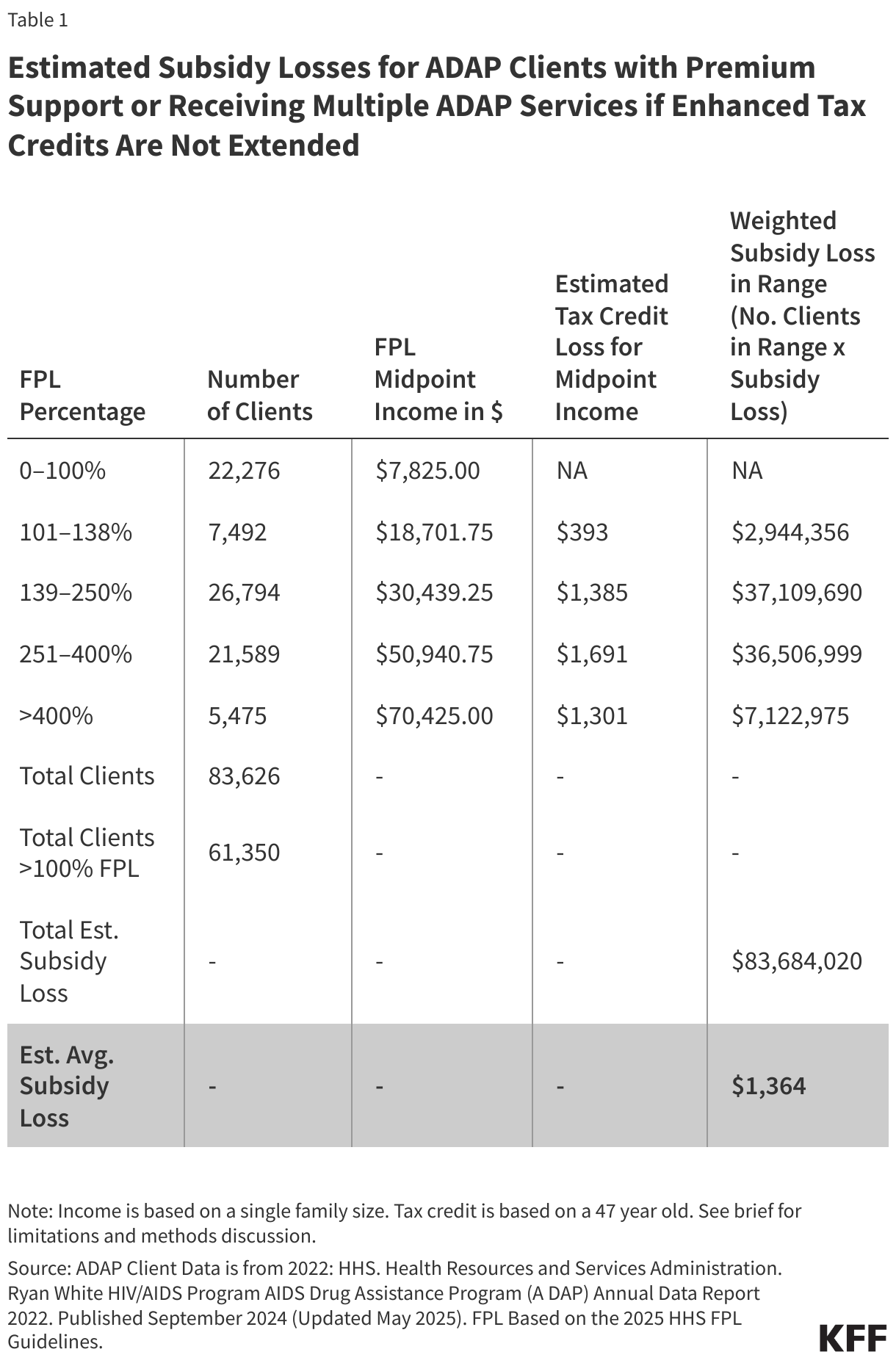

A typical ADAP shopper (with a mean age of 47 and in a single particular person household) receiving premium assist might anticipate to see an estimated further $1,364 in premium prices in 2026. This value could be borne by ADAPs and fluctuate by precise shopper demographics (i.e. age, earnings, household measurement and placement for these over 400% FPL who would lose the whole lot of their tax credit score), metallic degree enrollment, and the variety of purchasers the ADAP has enrolled within the Marketplaces. Completely different estimates will be generated using this tool. Total, this may probably signify a comparatively small improve in ADAP budgets. Nonetheless, considerations have already been raised that this coverage change, in addition to others which can be prone to occur soon because of the current reconciliation invoice, might be financially difficult for ADAPs. Moreover, sure state ADAPs, reminiscent of these with excessive market enrollment and people in non-expansion states are prone to be disproportionately impacted if enhanced tax credit. (See Strategies and Limitations.)

Elevated prices ensuing from expiring enhanced tax credit and better premiums, wouldn’t affect ADAPs evenly throughout the nation. Ranges of enrollment, variations in typical household earnings and age of purchasers, and sort of plan enrollment would affect how these modifications have an effect on ADAP budgets, amongst different elements. ADAPs with smaller shopper enrollment or much less sturdy insurance coverage buying packages could be extra sheltered and people with bigger shopper enrollment and sturdy insurance coverage help packages would prone to be tougher hit. It’s potential that ADAPs in non-Medicaid enlargement states might being particularly impacted. In enlargement states, many consumers with incomes 100-138% of the FPL could be enrolled within the Medicaid program whereas in non-expansion states, these purchasers could be extra prone to be enrolled in ADAP insurance coverage help by the ACA market. For example, the share of ADAP purchasers enrolled in Market plans (no matter whether or not ADAP is aiding with prices) is far increased for Florida (31%) and Georgia (25%), excessive prevalence non-expansion states, than in California (15%) or Illinois (11%), excessive prevalence enlargement states.

Moreover, as famous above, issuers are planning giant premium will increase for the approaching yr. ADAPs with purchasers enrolled in Market plans would nonetheless have some protections from these value hikes by premium tax credit. Even when the improved credit expire, purchasers 100%-400% FPL would nonetheless have the unique tax credit supplied by the ACA. Nonetheless, purchasers enrolled in off Market ACA compliant plans (about 9,600 purchasers in 2023) and purchasers with incomes over 400% FPL (7% of ADAP clients with premium assist or a number of varieties of ADAP assist in 2022) wouldn’t have any buffer towards these rising prices. Additional, ADAPs may additionally face increased prices if those that had been buying protection independently, discover will increase in premiums unaffordable and switch to this system for help.

Even comparatively small value will increase in ADAP budgets can problem their capacity to take care of their present ranges of providers and a few have raised questions on how they might reply to this and different future coverage modifications. ADAPs might reply in plenty of methods, a few of which might quantity to limiting entry to program providers or generosity and/or searching for various sources to complement federal funds:

- Value-containment methods might embrace altering the eligibility for this system – for instance decreasing the earnings eligibility degree – or additional limiting plans wherein purchasers can enroll. One other potential motion is making ADAP formularies for purchasers receiving direct drug help much less beneficiant or introducing extra utilization administration strategies like prior authorization or step-therapy. ADAPs might additionally introduce or cut back caps on their packages (or on drug utilization) and will additionally create ready lists. Ready lists have been used previously when program budgets have been strained however have been final cleared by infusion of supplemental federal funds in 2012.

- ADAPs confronted with elevated prices might try to complement ADAP earmark funding (funding devoted to ADAPs by Congress) with funding from different sources such because the state’s non-ADAP Ryan White fundings (Half B), funding from native county/metropolis Ryan White Grantees (Half A), different state/native funding, maximizing era of program earnings, and searching for deeper rebates from pharmaceutical corporations, amongst different actions. Nonetheless, if funding is shifted from Half B or different state or native funding (entities with already constrained budgets) to ADAPs, this might imply a discount of different public well being providers.

Past ADAPs, grantees of different “Elements” of the Ryan White Program are also permitted to use funding to assist shopper enrollment in medical insurance, together with in Market plans. Whereas this happens much less generally amongst different grantees than it does with ADAPs, some other grantees at present utilizing funding this fashion, would even be impacted by the above cost-increases ensuing from expiration of enhanced tax credit and will increase premiums for 2026.

Potential Impression of Coverage Adjustments on HIV Care

As described above, if these modifications happen, they’re prone to have an effect on each people with HIV and the packages individuals with HIV depend on. People might lose protection and/or face increased prices, and would possibly flip to Ryan White for help. To handle funding shortfalls because of these modifications, ADAPs might work to inject new funding into their packages however might additionally constrain present eligibility and advantages or limit enrollment.

Elevated premiums or sure modifications to ADAPs might result in enrollees being much less engaged with or fall out of HIV care and therapy. Greater out-of-pocket prices are a identified deterrent to care engagement. KFF has found that over-quarter (27%) of individuals with HIV who’re out-of-care say that a minimum of one barrier to care has been issues with cash or insurance coverage and of those that not too long ago missed an antiretroviral dose, almost 10% say issues have been as a barrier. Since HIV care and therapy engagement improves particular person well being and since viral suppression prevents transmission of HIV to others, monitoring entry to providers and security web program capability shifting forward will likely be essential, as will assessing the potential public well being affect, if individuals with HIV lose entry to care and therapy.

Lastly, whereas the potential expiration of tax credit is a looming main change on the well being coverage horizon, there are different important modifications coming that might affect care, protection, and packages for individuals with HIV. The current funds reconciliation invoice (HR1) makes a variety of changes to the health system that may cut back protection, some impacting the personal market however the largest, reshaping state Medicaid packages, the primary payer for HIV care within the U.S. These modifications too might put downward stress on ADAPs that are already working on budgets which have remained mostly flat for decades.

{kind=link}

Strategies and Limitations

Strategies: The estimated common earnings was generated primarily based on earnings and age date from the Health Resources and Services Administration (HRSA). Ryan White HIV/AIDS Program AIDS Drug Assistance Program (ADAP) Annual Data Report 2022. Published September 2024 (Updated May 2025). The info is predicated on 2022 ADAP shopper enrollment. Age and earnings information was examined for ADAP purchasers with premium assist and people getting a number of ADAP providers (probably together with premium assist). Age and earnings information within the HRSA report is offered in ranges with the variety of purchasers in every class. The vary midpoints have been recognized inside every class. For age, the estimated common age was calculated primarily based on a weighted common of age midpoints, excluding these over 65, a gaggle probably enrolled in Medicare. The typical age used on this evaluation was 47. For every earnings class incomes have been calculated primarily based off the vary midpoints utilizing the 2025 FPL guidelines from HHS. For the mid-point of every class for incomes above 100% FPL (these at present tax credit score eligible), the elevated value of expired tax credit was assessed utilizing the KFF calculator after which weighted primarily based on the variety of purchasers throughout the class (the weighted common estimated will increase for every vary are under). This evaluation used the “US common”, and was primarily based on a single particular person household measurement, representing a nationwide common of second-lowest value silver web page weighted by plan alternatives. Throughout all earnings classes we estimated a mean subsidy lack of $1,364. (See Desk 1.)

Limitations: There are a number of limitations with this estimate: Whereas these over 65 have been excluded from the typical age estimates, it was not potential to exclude the incomes of these over 65 from the earnings calculations. It’s potential Market enrollees have completely different demographics from these estimates which embrace purchasers receiving any ADAP insurance coverage premium (e.g. some purchasers receiving ADAP help for employer insurance coverage). It’s estimated that about 40,000 ADAP purchasers are enrolled in Market plans (the info above is for about 60,000 purchasers). Particularly, it’s potential that these earnings estimates are excessive on condition that these with employer protection are prone to have increased incomes than these with Market protection. The estimates additionally inlcude these receiving “a number of ADAP providers” which is assumed to inlcude these with premium help however might theoretically inlcude others. Averages might additionally obscure precise modifications in prices. Location of enrollment shouldn’t affect prices for many of these beneath 400% FPL due to the construction of the tax credit. Nonetheless, the US common used for the placement could also be imprecise for the 7% of enrollees assisted with premiums over 400% whose prices would fluctuate by location. As famous above, precise prices will fluctuate by shopper demographics (i.e. age, earnings, household measurement and placement for these over 400% FPL who would lose the whole lot of their tax credit score) in addition to shopper plan metallic degree enrollment. Further situations will be run utilizing the KFF calculator.