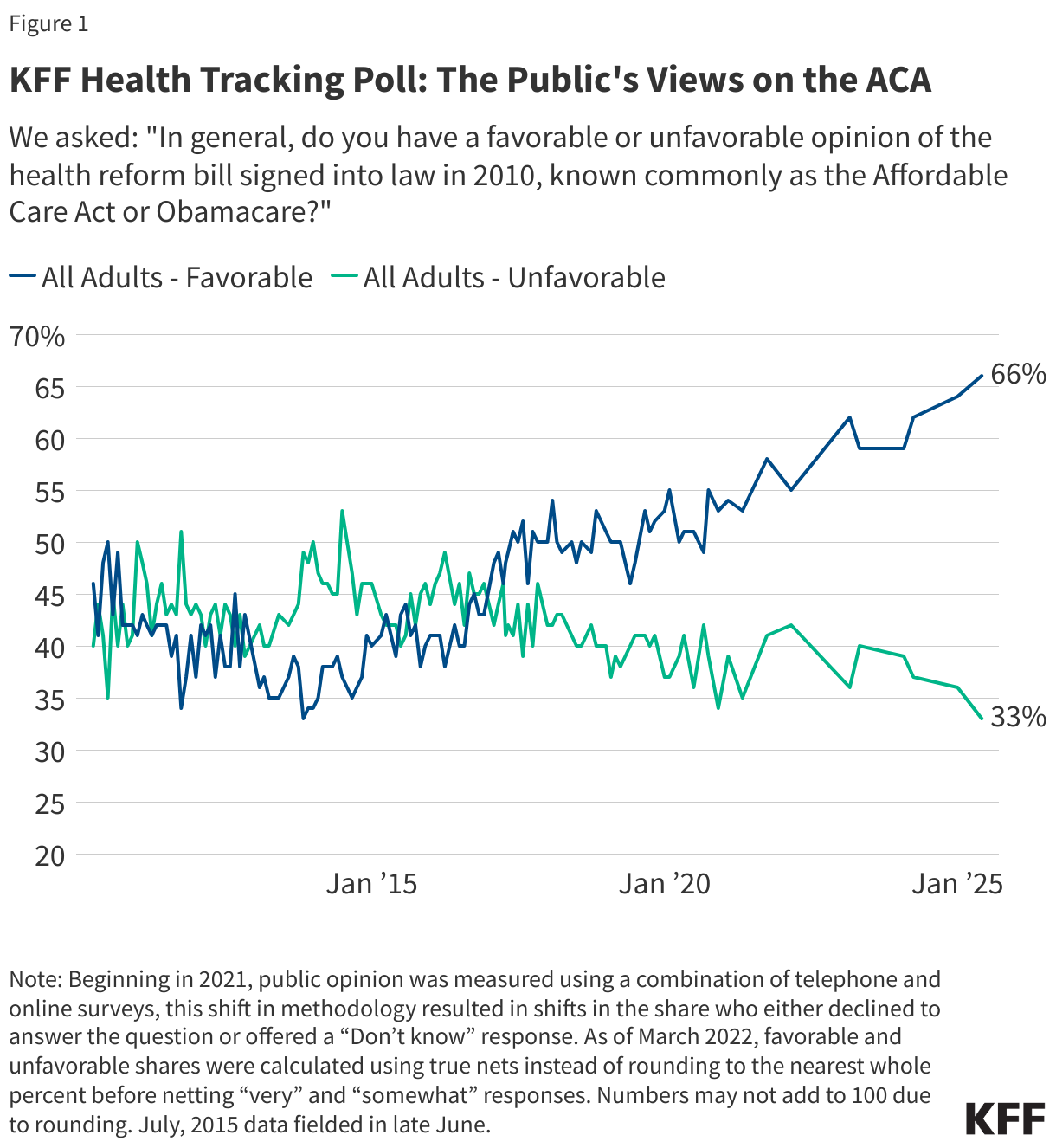

The ACA took full impact in 2014, with thousands and thousands gaining protection, however extra individuals viewed the law unfavorably than favorably, and repeal turned a Republican rallying cry within the 2016 marketing campaign. After the election of Donald Trump, a high-profile effort to repeal the legislation was ultimately defeated following a public backlash. The ACA repeal debate was a very good instance of the trade-offs inherent in all well being insurance policies. Republicans sought to cut back federal spending and regulation, however the end result would have been fewer individuals coated and weakened protections for individuals with pre-existing circumstances. KFF polling confirmed that the ACA repeal effort led to elevated public assist for the legislation, which persists in the present day.

Whereas President Trump failed in his first time period to repeal the ACA, his administration repealed the person mandate penalty, decreased federal funding for client help (navigators) by 84% and outreach by 90%, and expanded short-term insurance coverage that may exclude protection of preexisting circumstances.

In a wierd coverage twist, the Trump administration ended funds to ACA insurers to compensate them for a requirement to offer decreased price sharing for low-income sufferers. However, insurers responded by rising premiums, which in flip elevated federal premium subsidies and federal spending, seemingly strengthening the ACA.

Between President Trump’s presidential phrases, the Biden administration restored outreach funding and signed laws rising the premium tax credit that assist ACA Market enrollees pay their premiums, resulting in record enrollment and traditionally low uninsured charges.

The elevated premium tax credit are set to run out on the finish of 2025 until Congress and President Trump take motion. If these tax credit do expire, individuals buying backed protection will face significant increases of their month-to-month premium payments and a few could develop into priced out of the market.

President Trump’s second time period has already introduced federal coverage modifications that may considerably alter ACA Market operations, client protections, and premium tax credit score eligibility. Key modifications within the 2025 budget reconciliation law, corresponding to ending auto-renewals, eradicating compensation limits for tax credit when earnings rises, and tightening eligibility verification, are projected by the Congressional Funds Workplace (CBO) to lead to 2 million individuals turning into uninsured.